Switching bank account to reduce company carbon emissions

8 April 2024 (last updated 17 May 2024)

Tl;dr: Santander bank provided my business current account but they have high carbon emissions. I looked at the emissions of some other banks, and then chose Starling to switch to. 17 May: Switching is complete - I reckon my company’s emissions will reduce by nearly 400kgCO2e/year.

The carbon emissions of UK banks providing business accounts (detail)

The carbon emissions of UK banks providing business accounts (detail)

Problem: Santander has high carbon emissions

My current bank Santander has significant carbon emissions.

I want to reduce my emissions, so let’s see if I can find a better bank and switch to it.

Does it really make a difference? Yes.

Does it make a difference who you bank with? Yes:

- Emissions from banking and other financial services form a surprisingly large percentage of your organisation’s carbon footprint. Banking, pension and other financial services makes up about half of my company’s total emissions. (More on my company’s emissions soon.)

- Banks have massively varying emissions. This is mostly because some banks finance fossil fuels and other industries that create a lot of emissions. And others don’t.

My needs: lower emissions, still a bank

- Must haves: Greener. Lower emissions. Doesn’t fund fossil fuels. Does basic banking stuff: card, online/app, FSCS etc, integrates with Xero. Is a member of CASS so I can do the standard current account switch.

- Ideally also: Seems to be taking bold action on climate. Ethical policy and lending, pays fair tax, good governance, etc.

Method: find all of the bank’s emissions, and divide by their assets

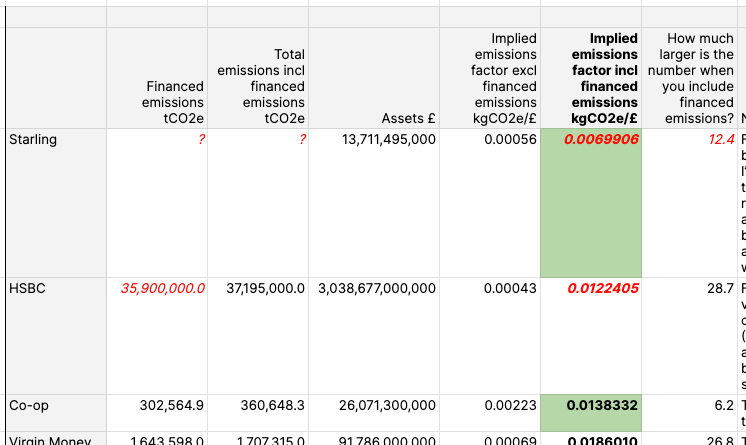

You can see my calculated numbers here.

I looked at a bunch of websites and made a shortlist of some banks, and removed the ones that don’t have business current accounts.

- Big/high street banks: HSBC, Lloyds, Barclays, Natwest/RBS. Plus my current bank Santander, Virgin Money.

- Ethical banks: Triodos (no business accounts), Co-op, Nationwide (no business accounts).

- Digital banks: Starling, Monzo, Tide, Revolut (not sure if this is a bank?), Tred (not a bank?)

- Other: Recognise

I used their annual or carbon reduction reports to look up their assets, scope 1-3 emissions, and financed emissions. Divided total scope 1-3 plus financed emissions by total assets to get an implied emissions factor, measured in kg emissions of CO2 equivalent per GBP pound.

If you multiply this implied emissions factor by the amount you have in your account, you get an emissions number you can then use in your own carbon emission measurements.

Finding the financed emissions is important. Banks invest in or lend to organisations who’ll use the money for activities that have emissions. These additional emissions aren’t usually reported in the standard GHG Protocol’s scope 1-3 emissions, but can be reported under the PCAF protocol.

The numbers can be massive. Example: my reading of Barclays bank’s annual report suggests that their scope 1-3 emissions are pretty good, but their financed emissions are ~1,000 times larger.

Digital or app-only banks like Starling and Monzo aren’t yet disclosing their financed emissions. Because their loan books tend to look less like the big 4 banks (heavy industry, agriculture, oil and gas etc) and more like the smaller banks like Co-op (mortgages, SME loans), I’ve done A Big Handwavy Guess at their financed emissions: I took the ratio between emissions without FE and emissions including FE for Co-op bank, doubled trebled it (to be conservative), and multiplied that by their emissions without FE. Horrible I know.

This is only one way to measure total emissions, and it relies completely on what a bank discloses. There are other approaches, some of which find higher emissions. Examples:

- MotherTree.

- Bank.green has a list and a proprietary methodology.

- And Co-op and Nationwide were listed in Sustainalytics’ ESG top-rated list.

Decision: Starling

You can see all the detail below, but here’s the summary: it was between Co-op and Starling, though I wonder if Tide would be up there too if I had newer numbers. They both look good, and I like what both say about emissions reduction. Co-op bank hasn’t been a mutual since 2013, and may be sold to a building society. Starling has the lowest emissions, though I’m guesstimating these because they don’t yet publish financed emissions. I don’t know what Co-op’s app is like, but I do know Starling’s as I’m a personal customer there already.

I’ve gone with Starling. If they publish financed emissions that look bad, I’ll move again.

17 May 2024 - how it’s going: Opening a bank account with Starling took under 24 hours and was easy. Activating a card, getting a transaction feed into my accounting system - also easy. Switching existing payments etc from Santander: done and no problems so far. Emissions reduction is nearly 400kgCO2e/year (much more detail on this soon).

Caveat: there are probably errors

- There are probably errors. But that’s ok: I’m not trying to scientifically prove which bank has which exact emissions. I’m only trying to be accurate enough to allow me to confidently switch bank. Corrections are welcome.

- Current accounts for businesses in the UK only. I’ve only reviewed current emissions - haven’t looked closely at bank’s reduction plans. Nor at business account fees and other account features. My measurements don’t attempt to split out business from non-business banking where a bank does both.

- Not all banks disclose their financed emissions, and my sense is that none measure things in exactly the same way. Some disclose their financed emissions in their annual report but do not put them into their headline numbers, perhaps because the numbers are massive. Small banks aren’t disclosing financed emissions at all yet - see my guesstimate in the method section above.

- Carbon emissions is a subset of a broader ethical category - I haven’t looked at social or governance factors.

The detail

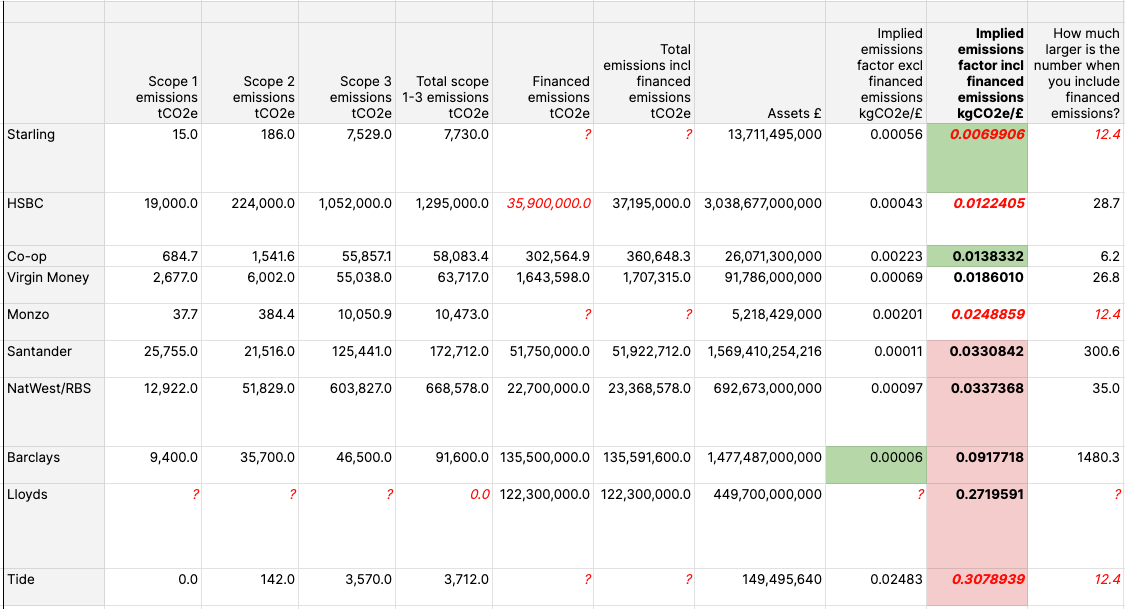

Carbon emissions of 10 UK banks

Carbon emissions of 10 UK banks

You can see my calculated numbers here.

The big banks disclose everything, sometimes in huge detail and complexity (HSBC, Barclays), sometimes just in complexity (Santander). Digital or app-only banks tend to have lower emissions because they have no branches, fewer employees and probably newer/less complex IT.

Big banks:

- Santander: bank accounts. Emissions - 2021 p84. Assets converted at exchange rate late Feb 24. 300x more finance emissions than standard scope 1-3!

- HSBC: bank accounts. Emissions p64ish and here p75, but nb different numbers in different docs… Financed emissions reported in a variety of metrics. Here I’m only using oil and gas (2023) and thermal coal (2020) because the other sectors aren’t reported in mtCO2e (sigh), so I believe these numbers are on the low side. (Tbh I’m discounting these numbers on feel as well - others like Banking On Climate Chaos list HSBC as a major funder of fossil fuels 2016-22.)

- Lloyds: bank accounts. Emissions: sustainability report p106, 115, 169-70 and methodology and here. Lloyds Scope 1-2: 22 mtCO2e. Scope 3: 43.9-68.9 (I’ve taken a midppoint of 56.4), Scottish Widows s1-2: 10.2. S3: 33.7. The finance emission numbers may include the bank’s S1-3 from own operations, it’s unclear. The numbers are terrible. Good: has resources to help business customers become more sustainable.

- Barclays: bank accounts. Emissions 2022, p187, financed emissions p81-2, assets p80. p88 “BlueTrack dashboard” has smaller numbers but I’ve gone with the bigger ones in p81-2. 1480x bigger! Note they don’t calculate financed emissions for all scopes or all GHGs, so the true number might be higher.

- Natwest/RBS: bank accounts and see also “green banking”. Emissions: annual report p58, and climate disclosures p68-9, - financed emissions includes 4mtco2e of estimate, p69 note 6 and ESG disclosures. You need to read all 3 to get the whole picture.

- Virgin Money: bank accounts, emissions - 2023 p36, 269, 285. The numbers quite easy to find in the annual report. S1-3 numbers much higher than Santander, but the financed emissions much lower. Owned by Nationwide soon.

Ethical banks:

- Triodos: probably would have been first choice, but has stopped doing business accounts :( The impact statements in the annual report feel like the strongest of the banks.

- Co-op: bank accounts here and here. Emissions. P41 of sustainability report shows they include financed emissions (mortgages) of 302,564tCO2e (which is ~6x more than S1-3 without lending ~58ktCO2e). Most other banks do not put their financed emissions number front and centre like this. Owned by Coventry Building Society soon.

- Nationwide: emissions could have been a good choice, has no business account :(

Digital banks:

- Starling: bank accounts. Emissions and reduction plan: “For now, we haven’t included emissions relating to loans and investments in our Scope 3 carbon footprint breakdown as these are worked out separately with the Partnership for Carbon Accounting Financials (PCAF)”. Also here and good early action on greener cards etc.

- Monzo: bank accounts. Emissions but no public carbon emissions/reduction plan? Or mention of financed emissions. Also. Uses Watershed.

- Tide: bank accounts - Tide uses Clearbank as its banking layer. Emissions and this. Strong carbon statements (biochar: nice), however poor calculated emission numbers. This might be because Tide’s still in early growth mode, or that I’m over-estimating carbon intensity because I’m using a number for assets from Dec 2022 reporting to Companies House (perhaps this will have changed a lot 12m later due to organic growth and acquisitions - and growth in assets may reduce emissions intensity). I couldn’t find a mention of financed/facilitated emissions, so emissions estimated with Big Handwavy Guess method. Feels like it’s worth keeping an eye on Tide: I think its numbers will improve this year.

- Revolut: bank account and here. I can’t tell if Revolut is a bank or not.

- Tred: an e-money/payment card? and costs 196/year which includes carbon accounting. Emissions. Not actually a bank, but maybe an interesting add-on.

OK that’s it.

For more like this:

climate transformation email newsletter: