Show them it’s here already

4 September 2024

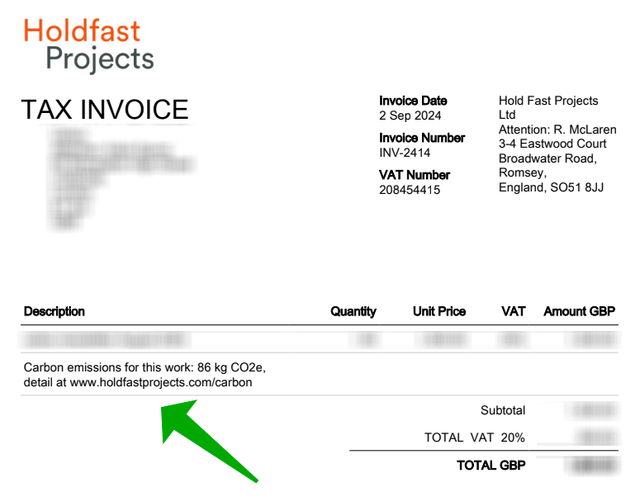

My proposals and invoices now include carbon emissions data, because even the smallest public acts might encourage others to take action too. My

Rams: The time of thoughtless design for thoughtless consumption is over

3 June 2024

My proposals and invoices now include carbon emissions data, because even the smallest public acts might encourage others to take action too. My

Rams: The time of thoughtless design for thoughtless consumption is over

3 June 2024

3 June 2024 These screengrabs are from Gary Hustwit’s documentary Rams and its trailer video. If the video is paywalled, there are a couple of clips

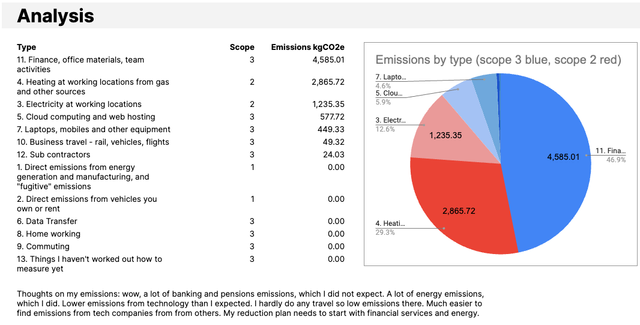

9.79 tonnes CO2e per year

17 May 2024

3 June 2024 These screengrabs are from Gary Hustwit’s documentary Rams and its trailer video. If the video is paywalled, there are a couple of clips

9.79 tonnes CO2e per year

17 May 2024

17 May 2024, updated 25 October 2024. My company’s total carbon emissions are 9.79 tonnes CO2e per year, for the year 1 March 2023 - 29 February

The leap from experience to trust

18 April 2024

17 May 2024, updated 25 October 2024. My company’s total carbon emissions are 9.79 tonnes CO2e per year, for the year 1 March 2023 - 29 February

The leap from experience to trust

18 April 2024

18 April 2024 You used to be able to confidently predict that the future would look more or less like today: many things getting a bit better, some

Switching bank account to reduce company carbon emissions

9 April 2024

18 April 2024 You used to be able to confidently predict that the future would look more or less like today: many things getting a bit better, some

Switching bank account to reduce company carbon emissions

9 April 2024

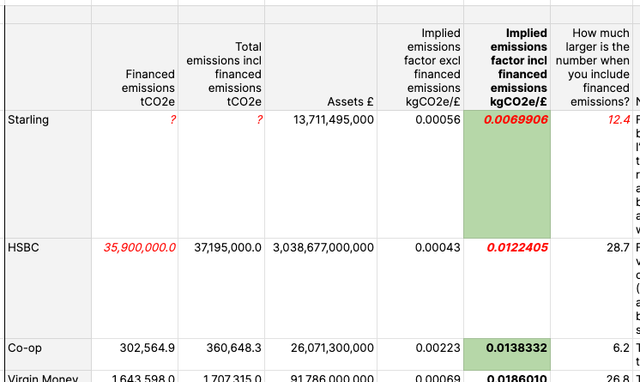

8 April 2024 (last updated 17 May 2024) Tl;dr: Santander bank provided my business current account but they have high carbon emissions. I looked at

Climate change is an engineering challenge

27 March 2024

8 April 2024 (last updated 17 May 2024) Tl;dr: Santander bank provided my business current account but they have high carbon emissions. I looked at

Climate change is an engineering challenge

27 March 2024

27 March 2024 Generative Engineering reduces the time and cost of engineering individual parts or full systems by generating and testing thousands

Dirty internet: carbon aware websites

11 March 2024

27 March 2024 Generative Engineering reduces the time and cost of engineering individual parts or full systems by generating and testing thousands

Dirty internet: carbon aware websites

11 March 2024

11 March 2024, updated 26 September 2024. Two ways websites become more aware of their emissions: Some websites that react to the current carbon

How to play the LinkedIn blogging game

31 January 2024

31 January 2024 Writing this down because I can never remember. This seems to be how to publish on LinkedIn to get better engagement, comments,

3 stories to complete the Co-op Digital newsletter

28 October 2023

11 March 2024, updated 26 September 2024. Two ways websites become more aware of their emissions: Some websites that react to the current carbon

How to play the LinkedIn blogging game

31 January 2024

31 January 2024 Writing this down because I can never remember. This seems to be how to publish on LinkedIn to get better engagement, comments,

3 stories to complete the Co-op Digital newsletter

28 October 2023

28 Oct 2023 The Co-op Digital newsletter occasionally had stories in it, tiny fictions to explore what retail and the world might look like as

Words that work for digital + climate transformation

26 September 2023

Hello, I’m Rod McLaren. I’m a writer. If you thought digital transformation was spiky and disruptive, wait til you see climate transformation. It is

When is something ready to publish?

15 September 2023

15 Sep 2023 Honestly, it’s never ready. Publishing the new website - or even just a blog post - often feels like an uncomfortable step. It’s

Technology eating retail: stories

19 August 2022

19 Aug 2022 The Co-op Digital newsletter occasionally has some fiction in it, tiny story fragments to explore what retail might look like as

(Fr)agile

9 June 2022

2 Jun 2022 I helped Stripe Partners write a couple of provocations about how “agile” works today, now that it has evolved from a test-iterate

Writing questions

16 December 2021

16 Dec 2021 These are some of the questions I ask myself when writing pieces to unpack tech news, explain ideas, persuade a reader, present an idea

Carbon transformation

8 November 2021

5 Nov 2021 These days it feels like many consultancies say they do “digital transformation”. Partly this is a marketing thing - it has been a useful

How to become a digital writer or content designer

13 October 2021

13 Oct 2021 A friend messages, asking for some advice on how you become a writer/content designer in tech. This is a good question. I think writing

Public Digital’s website

16 December 2020

28 Oct 2023 The Co-op Digital newsletter occasionally had stories in it, tiny fictions to explore what retail and the world might look like as

Words that work for digital + climate transformation

26 September 2023

Hello, I’m Rod McLaren. I’m a writer. If you thought digital transformation was spiky and disruptive, wait til you see climate transformation. It is

When is something ready to publish?

15 September 2023

15 Sep 2023 Honestly, it’s never ready. Publishing the new website - or even just a blog post - often feels like an uncomfortable step. It’s

Technology eating retail: stories

19 August 2022

19 Aug 2022 The Co-op Digital newsletter occasionally has some fiction in it, tiny story fragments to explore what retail might look like as

(Fr)agile

9 June 2022

2 Jun 2022 I helped Stripe Partners write a couple of provocations about how “agile” works today, now that it has evolved from a test-iterate

Writing questions

16 December 2021

16 Dec 2021 These are some of the questions I ask myself when writing pieces to unpack tech news, explain ideas, persuade a reader, present an idea

Carbon transformation

8 November 2021

5 Nov 2021 These days it feels like many consultancies say they do “digital transformation”. Partly this is a marketing thing - it has been a useful

How to become a digital writer or content designer

13 October 2021

13 Oct 2021 A friend messages, asking for some advice on how you become a writer/content designer in tech. This is a good question. I think writing

Public Digital’s website

16 December 2020

Public Digital’s new website, Oct 2020 I wrote the words for the new Public Digital website. Public Digital (PD) works with governments and

How to find your books

30 October 2020

Public Digital’s new website, Oct 2020 I wrote the words for the new Public Digital website. Public Digital (PD) works with governments and

How to find your books

30 October 2020

30 Oct 2020 Matt Webb wrote about using an app called Memos to make his bookshelves searchable: find where that book is by searching your photos.

Data is a material for building with

16 October 2019

I believe that architects and engineers must think of data as a material. Start with visibility: disclose data collection in a way that makes it

Why Co-op Digital writes a newsletter

12 June 2019

30 Oct 2020 Matt Webb wrote about using an app called Memos to make his bookshelves searchable: find where that book is by searching your photos.

Data is a material for building with

16 October 2019

I believe that architects and engineers must think of data as a material. Start with visibility: disclose data collection in a way that makes it

Why Co-op Digital writes a newsletter

12 June 2019

I wrote a bit about the Co-op Digital newsletter for the Co-op blog, how it started and how it’s put together etc. The clever Amy McNichol did the

Next page

I wrote a bit about the Co-op Digital newsletter for the Co-op blog, how it started and how it’s put together etc. The clever Amy McNichol did the

Next page